For years, big technology companies have held immense control over user data. Every click, search, and online interaction is collected, stored, and often monetized without users having a clear understanding of how their information is being used. Concerns over privacy, security, and data ownership have grown significantly, pushing individuals and businesses to seek alternatives. This is where blockchain technology is making a difference. It provides a decentralized approach, ensuring that user data remains private, secure, and under individual control.

Understanding How Big Tech Controls User Data

Big tech companies, including social media platforms, search engines, and cloud service providers, collect vast amounts of user data. This data is used for targeted advertising, improving user experiences, and sometimes even sold to third parties. The key concerns with this centralized control include:

- Lack of Transparency: Users often do not know how their data is being used.

- Data Breaches: Centralized databases are frequent targets of cyberattacks.

- Monetization Without Consent: Companies profit from user data without proper compensation or permission.

- Censorship and Manipulation: Platforms can filter or manipulate information based on their interests.

How Blockchain Offers a Decentralized Solution

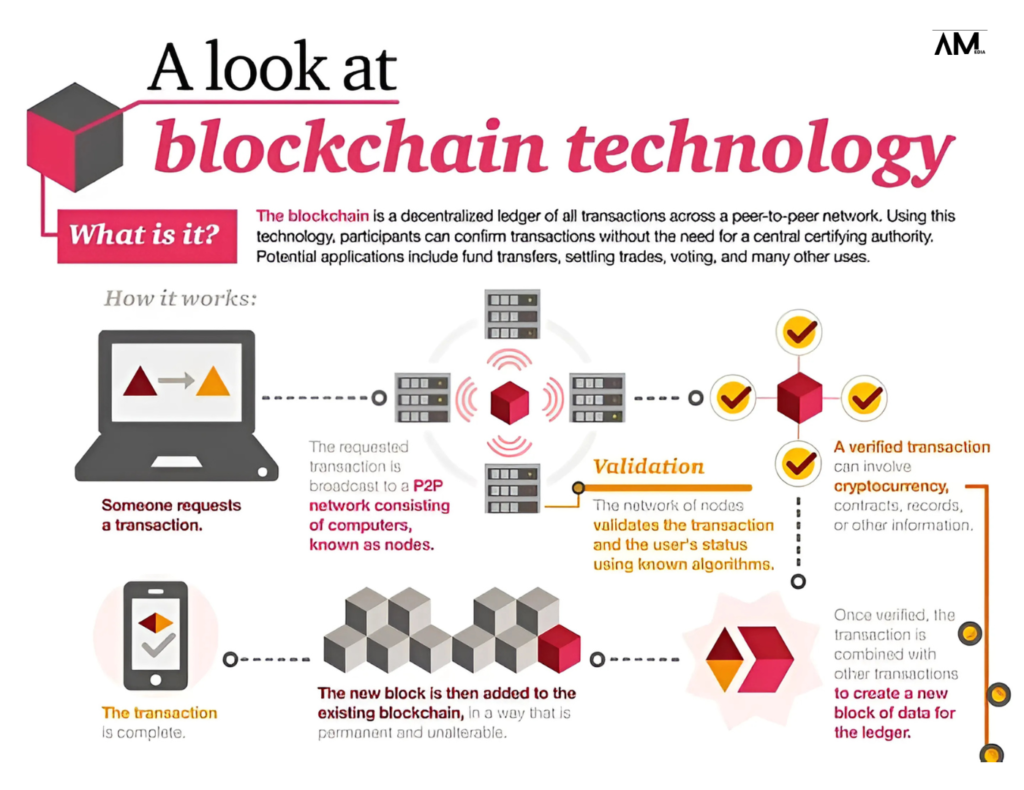

Blockchain technology provides an alternative model that eliminates the need for centralized control. Instead of data being stored on a single server controlled by a corporation, blockchain distributes data across a network of computers. This approach offers several advantages:

- Ownership and Control: Users own their data and decide who can access it.

- Transparency: Every transaction on a blockchain is recorded, providing a clear view of data interactions.

- Security: Decentralization reduces the risk of hacking since there is no central point of failure.

- No Intermediaries: Transactions and data exchanges happen directly between users without the need for a central authority.

Key Areas Where Blockchain is Disrupting Big Tech’s Data Control

1. Social Media and Content Sharing

Social media platforms collect and monetize user data. Blockchain-based social networks, such as Steemit and Minds, allow users to share content while maintaining ownership of their data. These platforms also provide token-based incentives, rewarding users for their contributions.

2. Decentralized Cloud Storage

Big tech companies offer cloud storage services that are convenient but come with concerns about privacy and data ownership. Blockchain-based storage platforms like Filecoin and Storj distribute data across a network of computers, ensuring no single entity has full control over user files.

3. Identity Management

Online identity verification often requires users to provide personal details to centralized companies, making them vulnerable to data theft. Blockchain-based identity systems allow users to verify their identity securely without revealing unnecessary personal details.

4. Data Marketplaces

Companies profit from user data, but individuals rarely benefit. Blockchain-based data marketplaces allow users to monetize their data on their terms. Platforms like Ocean Protocol enable secure data exchanges where users can sell access to their data while maintaining control over it.

5. Decentralized Finance (DeFi)

Traditional financial services rely on big tech for data storage and transactions. Blockchain-based finance eliminates intermediaries, providing direct access to financial services without the need for banks or tech companies.

Benefits of Blockchain Over Big Tech’s Model

| Feature | Big Tech Model | Blockchain Model |

|---|---|---|

| Data Ownership | Controlled by companies | Controlled by individuals |

| Security | Prone to breaches | Highly secure due to decentralization |

| Transparency | Limited | Full visibility on transactions |

| Monetization | Companies profit from user data | Users can monetize their own data |

| Access Control | Centralized | Distributed and permissioned |

Challenges and Limitations of Blockchain Adoption

While blockchain presents a strong alternative, it is not without its challenges:

- Scalability Issues: Blockchain networks can be slower than centralized systems.

- Regulatory Concerns: Governments are still figuring out how to regulate blockchain-based solutions.

- Complexity: Many users are unfamiliar with blockchain technology, making adoption slow.

- Energy Consumption: Some blockchain networks require significant computational power.

Important Facts About Blockchain and Data Privacy

- Over 90% of companies are exploring blockchain for data security.

- The global blockchain market is expected to reach $163 billion by 2029.

- Data breaches cost businesses an average of $4.24 million per incident.

- Decentralized applications (dApps) provide more privacy than traditional apps.

How Businesses and Individuals Can Benefit from Blockchain

For Individuals:

- Use blockchain-based social media platforms for content sharing.

- Store personal data on decentralized cloud platforms.

- Use blockchain-based identity verification systems.

- Monetize personal data on decentralized marketplaces.

For Businesses:

- Implement blockchain-based customer data protection measures.

- Explore decentralized cloud storage for improved security.

- Use blockchain for transparent financial transactions.

- Invest in blockchain-based identity verification to prevent fraud.

The Future of Blockchain in Data Privacy

As blockchain technology advances, its adoption in data privacy and security will increase. Governments and organizations are already investing in decentralized solutions to protect user data. In the coming years, blockchain is expected to:

- Replace traditional data storage models with decentralized alternatives.

- Provide better control over online identities.

- Reduce reliance on big tech companies for digital transactions.

- Improve data security in industries like healthcare, finance, and e-commerce.

Conclusion

Big tech companies have controlled user data for decades, often without full transparency or consent. Blockchain is emerging as a powerful alternative, offering security, ownership, and control to users. While challenges remain, the shift towards decentralized solutions is inevitable. Businesses and individuals looking to safeguard their data should consider blockchain-based platforms as a step towards a more secure and fair digital future.

Editor’s Choice:

A Decade Of Digital Disruption: The Evolution Of Marketing In The Digital Age & Future Trends

The L.O.V.E. 4-Step Email Copywriting Framework: Connections, Trust & Conversion

Why T-Shaped Marketers Hold The Key To Success In The New Marketing Age